What is the Europe Cold Plasma Equipment Market Overview – Definition, scope, and significance?

The Europe Cold Plasma Equipment market comprises devices that generate non‑thermal plasma for medical, industrial, and research applications. Cold plasma, also known as non‑equilibrium plasma, operates at near‑ambient temperatures, allowing direct interaction with heat‑sensitive materials such as human tissue. The market’s scope covers atmospheric‑pressure and low‑pressure systems, serving sectors like wound healing, blood coagulation, oncology, dentistry, and emerging niche uses. Its significance lies in offering sterilization, tissue regeneration, and minimally invasive therapeutic options that align with Europe’s strong regulatory framework, high healthcare spending, and commitment to innovative medical technologies.

What are the Europe Cold Plasma Equipment Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising demand for advanced wound care, growing prevalence of chronic diseases, and supportive EU policies promoting medical innovation. The shift toward non‑antibiotic antimicrobial solutions further fuels adoption. Restraints stem from high capital costs, limited long‑term clinical data, and stringent certification processes that can delay product launch. Challenges involve integrating plasma devices into existing clinical workflows and ensuring practitioner training. Opportunities arise from expanding applications in oncology (e.g., tumor ablation), personalized dentistry, and potential partnerships with biotech firms developing plasma‑enhanced drug delivery platforms.

What are the Europe Cold Plasma Equipment Market Growth Trends?

Current trends show a rapid transition from laboratory prototypes to commercially viable systems, especially atmospheric cold plasma devices that require minimal infrastructure. Companies are increasingly focusing on modular, user‑friendly designs to broaden hospital adoption. There is a noticeable trend toward combining plasma treatment with nanomedicine, creating hybrid therapies for cancer and regenerative medicine. Additionally, the rise of tele‑medicine and outpatient clinics is prompting the development of portable plasma units, supporting decentralized care models across Europe.

How did COVID‑19 impact the Europe Cold Plasma Equipment Market and what is the recovery trajectory?

The pandemic temporarily slowed elective procedures, reducing short‑term equipment sales, but it also highlighted the need for effective infection control, boosting interest in plasma‑based sterilization. Supply chain disruptions were mitigated by Europe’s strong local manufacturing base. Post‑2020, demand rebounded as hospitals resumed routine care and accelerated adoption of technologies that reduce antibiotic use. The recovery trajectory is positive, with market confidence restored and investment in research resuming, setting the stage for accelerated growth.

What does the Europe Cold Plasma Equipment Market Competitive Landscape look like?

The competitive landscape is characterized by a mix of specialist manufacturers and larger conglomerates expanding into plasma technology. Major players such as Adtec, Bovie Medical, Europlasma NV, and Plasmatreat GmbH dominate key segments, offering both atmospheric and low‑pressure systems. Recent years have seen strategic collaborations, joint ventures, and selective acquisitions aimed at broadening product portfolios and geographic reach. While market concentration remains moderate, the pace of innovation ensures ongoing competitive pressure.

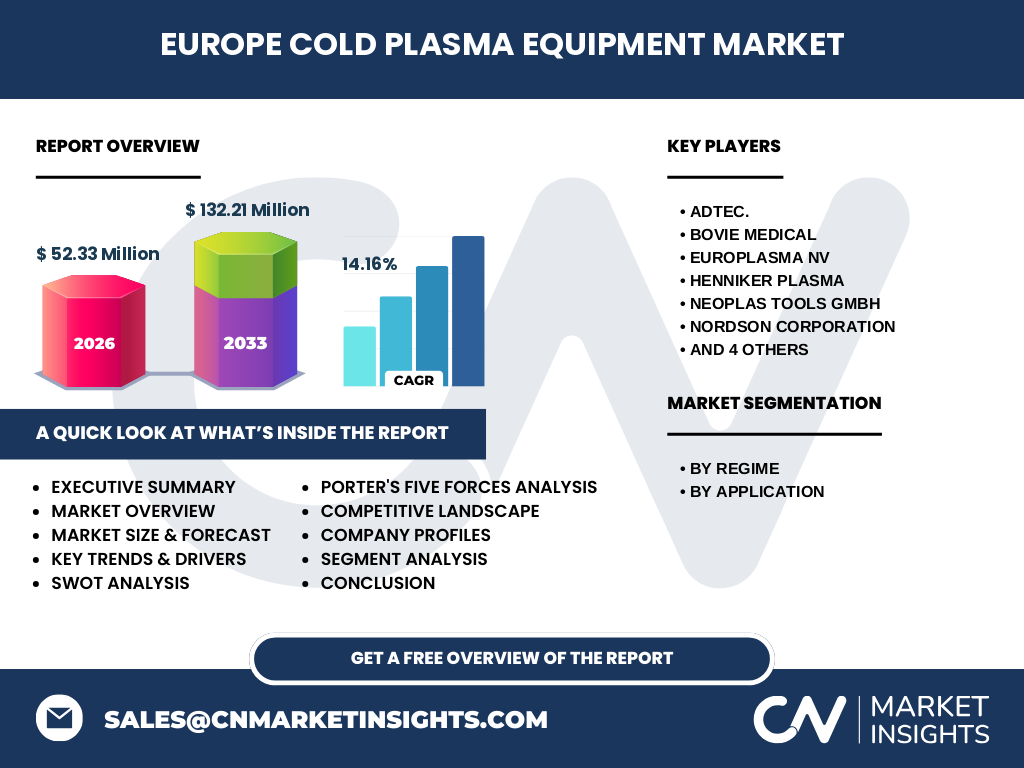

What are the key findings in the Executive Summary of the Europe Cold Plasma Equipment Market?

The market is projected to grow from a 2026 valuation of €52.33 million to €132.21 million by 2033, delivering a robust CAGR of 14.16 %. Growth is propelled by expanding clinical applications, especially in wound care and oncology, and by supportive regulatory environments. Atmospheric cold plasma devices are gaining market share due to ease of integration, while low‑pressure systems retain importance for specialized research. The competitive field is dynamic, with leading firms investing heavily in R&D and partnerships to capture emerging opportunities.

What is the Europe Cold Plasma Equipment Market Forecast for 2025‑2032?

Based on the provided CAGR of 14.16 %, the market is expected to maintain strong double‑digit expansion through 2032. The trajectory indicates a steady rise in unit shipments, driven by heightened clinical adoption and advancements in device portability. Forecasts suggest that atmospheric cold plasma equipment will lead growth, while low‑pressure solutions will sustain niche demand in research institutions. The overall market environment remains favorable, underpinned by continued funding for innovative medical technologies within the EU.

What is the Europe Cold Plasma Equipment Market Size and Share by Segmentation?

By regime, the market splits into atmospheric cold plasma equipment and low‑pressure cold plasma equipment. Atmospheric systems are gaining a larger share due to lower installation complexity and suitability for point‑of‑care settings. By application, wound healing holds the biggest share, followed by blood coagulation, cancer treatment, dentistry, and other emerging uses. This segmentation reflects the clinical priority for faster healing solutions and the expanding research into plasma‑mediated therapies.

What is the Global Europe Cold Plasma Equipment Market Size and Share by Region?

Europe represents a key region within the global cold plasma equipment landscape, contributing a substantial portion of the overall market because of its advanced healthcare infrastructure and strong R&D ecosystem. While exact global figures are not disclosed, Europe’s market size of €52.33 million in 2026 and projected growth to €132.21 million by 2033 indicate a leading role, especially when compared with other mature markets in North America and Asia‑Pacific.

What does the Regional Analysis of the Europe Cold Plasma Equipment Market reveal?

The regional analysis highlights Western Europe—particularly Germany, France, and the United Kingdom—as the primary hubs for sales and R&D activities, driven by high hospital density and supportive innovation incentives. Northern European countries, such as Sweden and Denmark, are notable for early adoption of plasma‑based wound care protocols. Southern and Eastern European markets exhibit slower but accelerating uptake, buoyed by growing public‑private partnerships and increasing healthcare expenditures.

Who are the leading companies in the Europe Cold Plasma Equipment Market and what are their strategies?

Key players include Adtec, Bovie Medical, Europlasma NV, Henniker Plasma, Neoplas tools GmbH, Nordson Corporation, Plasmatreat GmbH, Tantec A/S, TheraDep Technologies, and terraplasma medical GmbH. Strategies focus on product diversification (offering both atmospheric and low‑pressure platforms), expanding clinical evidence through trials, and forging strategic alliances with hospitals and research institutes. Many firms are also pursuing geographic expansion within the EU and investing in digital platforms to support remote monitoring and data analytics for plasma treatments.

How does Porter’s Five Forces analysis apply to the Europe Cold Plasma Equipment Market?

Threat of new entrants is moderate; high R&D costs and regulatory hurdles act as barriers, yet niche innovators can enter with specialized solutions. Bargaining power of suppliers is low to moderate because component suppliers (e.g., power electronics) are fragmented. Bargaining power of buyers is growing as hospitals seek cost‑effective, evidence‑based technologies, prompting manufacturers to offer value‑added services. Threat of substitutes remains limited; while traditional therapies (antibiotics, laser) exist, plasma offers unique non‑thermal benefits. Competitive rivalry is intense, with multiple firms racing to secure patents, clinical data, and market share.

What is the SWOT analysis of the Europe Cold Plasma Equipment Market?

Strengths: Strong clinical demand, supportive EU policies, and a broad portfolio of applications. Weaknesses: High upfront cost and limited long‑term outcome data. Opportunities: Expansion into oncology, portable devices for outpatient care, and collaborations with biotech firms. Threats: Regulatory delays, potential competition from emerging technologies, and reimbursement uncertainties.

What does the Europe Cold Plasma Equipment Market Value Chain look like?

The value chain begins with research institutions developing plasma generation technologies, followed by component suppliers (high‑frequency generators, electrodes). Manufacturers then assemble and certify equipment, integrating software for treatment protocols. Distribution channels include direct sales to hospitals, specialty medical distributors, and leasing firms. After‑sales services—maintenance, training, and data analytics—complete the chain, fostering long‑term relationships and recurring revenue streams.

What key investment insights can be drawn for the Europe Cold Plasma Equipment Market?

Investors should focus on companies with strong clinical trial pipelines and proven regulatory approvals, as these assets reduce time‑to‑market risk. Strategic investments in atmospheric plasma platforms offer higher scalability and faster adoption. Partnerships with healthcare providers that provide real‑world evidence can enhance valuation. Additionally, funding cross‑border collaborations that merge plasma technology with advanced drug delivery or digital health solutions presents a high‑growth avenue.

What is the concluding summary of the Europe Cold Plasma Equipment Market?

The Europe Cold Plasma Equipment market is on a clear growth trajectory, underpinned by a 14.16 % CAGR and a projected market size of €132.21 million by 2033. Clinical demand, especially for wound healing and emerging oncology applications, drives expansion, while atmospheric devices dominate due to practicality. Competitive dynamics are robust, encouraging continuous innovation. The market’s outlook remains positive, offering compelling opportunities for manufacturers, investors, and healthcare systems seeking advanced, non‑thermal therapeutic options.

What research methodology was employed for this market study?

The study combines primary interviews with key industry stakeholders—including clinicians, manufacturers, and regulatory experts—and secondary data from scientific publications, market reports, and company filings. Quantitative modeling applies the disclosed CAGR to project future values, while qualitative analysis interprets trends, competitive dynamics, and regulatory impacts. Cross‑validation ensures consistency with publicly available financial and market information.

What is the scope of this research and its limitations?

The scope encompasses Europe‑wide cold plasma equipment covering both atmospheric and low‑pressure regimes and five primary applications. Geographic focus includes major Western, Northern, Southern, and Eastern European markets. Limitations arise from the reliance on publicly disclosed financial figures and the absence of granular country‑level revenue breakdowns, which may affect precise market share calculations.

Which key companies have recent developments in the Europe Cold Plasma Equipment Market?

Recent announcements include Adtec’s launch of a next‑generation atmospheric plasma system for rapid wound decontamination, Bovie Medical’s acquisition of a low‑pressure plasma research unit to strengthen its oncology pipeline, and Europlasma NV’s partnership with a French university for clinical trials in dental plaque reduction. Plasmatreat GmbH introduced a portable plasma handheld device targeting bedside blood coagulation, while TheraDep Technologies secured EU funding for a collaborative cancer‑treatment project. These developments reflect the market’s dynamic innovation environment.